'There is a lack of diversity at senior levels in Irish financial firms. That needs to change'

Central Bank research shows four-fifths of all senior financial positions in Ireland are being filled by men.

THERE IS A lack of diversity at senior levels across financial services firms operating in Ireland.

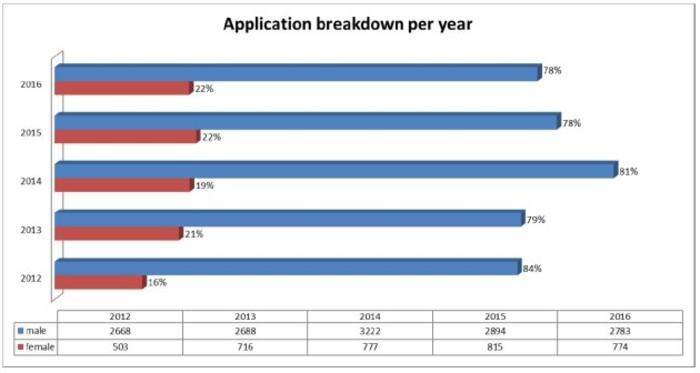

The Central Bank of Ireland today published data showing that, since 2012, 80% of the nearly 18,000 applications for regulatory approval for senior level roles in regulated financial services firms have been for men.

This data was gathered as part of the Central Bank’s fitness and probity regime, which requires pre-approval for the most senior and high-impact roles in financial services firms.

For the reasons discussed below, we are concerned that this lack of diversity potentially increases financial stability and consumer protection risks and, therefore, needs to be addressed.

It is worth noting that the data we have published focuses on only one aspect of diversity, albeit a very important one – gender, as this is the reliable data we have.

What does the data show?

The vast majority of senior management role holders and board members in financial services firms operating in Ireland are men. This was the case before the onset of the financial crisis and is the case today, albeit with some marginal improvements.

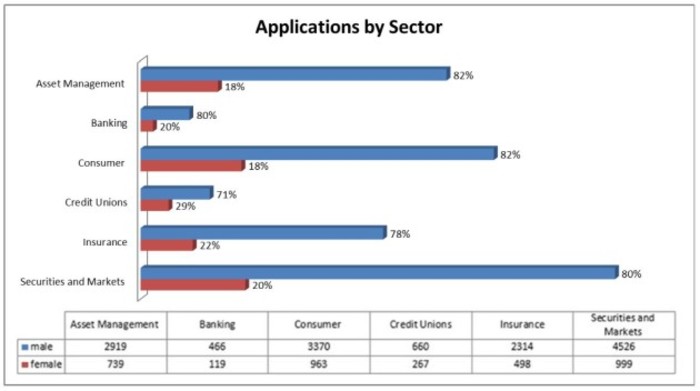

Across financial services firms, 80% of applicants for regulatory approval have been for men. There are some differences in different sectors, but with the exception of credit unions (at 29% women), these are not significant.

The low levels of gender diversity are concerning. Anecdotal experience suggests that for many other aspects of diversity, beyond gender, the situation may be worse.

Strikingly, beneath the headline numbers, there is an even greater gender imbalance for roles that are revenue-generating. Furthermore, women comprised 12% of applicants for chief executive roles, 12% of applicants for board chair roles, 15% of applicants for executive director roles and 18% of applicants for non-executive director roles.

It is important to note that the percentage of applicants does not mean the percentage of people applying to financial firms for those roles – it is the percentage of people who have been offered those roles by financial services firms and need Central Bank approval before they can start.

So why does this matter?

We are concerned that this lack of diversity is negatively affecting the behaviour and culture in financial services firms, their decision-making and risk management and consequentially increasing the risk of poor consumer protection outcomes and financial stability issues.

To put this into context, there were many factors that led to the global financial crisis and its acute impacts in Ireland. Governance, risk management and cultural issues all contributed, together with collective group-think issues.

These meant the prevailing assumptions regarding the economy and financial services firms’ business models often went unchallenged.

The legacies of the crisis are still very much with us. However, significant progress has been made in improving the financial strength of financial services firms and repairing weaknesses in governance and risk management arrangements.

The rule books underpinning the regulation and supervision of all sectors have been re-written and strengthened. However, it is more difficult to legislate to improve behaviour and culture, the effectiveness of decision-making, the approach to challenge within firms, and to reduce the risk of group-think.

Importantly, there is a strong and growing body of evidence that greater diversity, in all senses of the word, at senior management levels can positively impact in these areas - improving the behaviour and culture within firms, the process and quality of decision-making, and on the level and effectiveness of internal challenge.

Smarter risks

Research suggests that firms with more diverse senior management do not take less risk, but those risks that they do take are more carefully examined and challenged. This is consistent with evidence that diversity is positively correlated with firms’ success and reducing the risk of failure.

Diversity in all its forms is, therefore, an issue that should be of concern to regulators and supervisors, at both a micro, firm specific level and in looking across the system as a whole.

There are regulatory requirements for financial services firms in many sectors (including banking and insurance) to have diversity policies. Our review of a sample of these policies shows, in the main, a worrying lack of ambition.

In many cases internal targets have been set that are already being met, many lack accountability, and there is little evidence that progress against them is being monitored.

Remarkably, for two large financial services firms, their diversity policies were exactly the same, word for word, with the exception of the names of the firms and some of the targets they had.

Notwithstanding these issues, there are financial services firms that have a healthy gender balance, with applications among certain banks and insurance companies at 44% and 45% female applicants over the past five years.

There are financial services firms that have board-sponsored diversity policies and programmes that demonstrate that diversity is a priority; have set out ambitious targets and a credible plan and timeline for achieving greater diversity; and can provide evidence that these targets, and the effective implementation of these plans, are reviewed and monitored and have clear senior-level ownership.

There are also sector-wide initiatives that are focusing on addressing these issues, which the Central Bank is actively participating in – including to support the development and delivery of our internal diversity and inclusion programme, which aims to continue to enhance our own approach.

Nonetheless, the continued and evident lack of diversity at the most senior levels across the financial services industry in Ireland needs to be addressed. We intend to enhance our engagement with firms on this important issue. We will challenge companies on it and we will expect to see greater progress and commitment from all regulated firms.

Ed Sibley is director of credit institutions supervision at the Central Bank of Ireland.

If you want to share your opinion, advice or story, email opinion@fora.ie.